Business

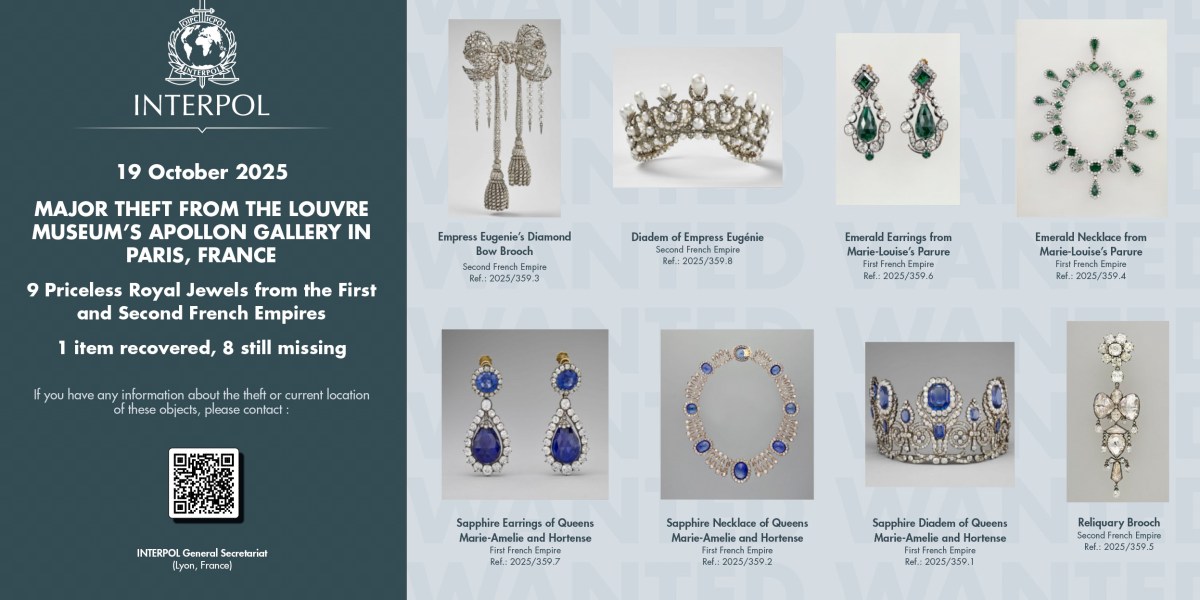

Louvre jewels mystery deepens: Experts warn what could happen to the $100 million in missing artifacts now

Business

Trust has become the crisis CEOs can’t ignore at Davos, as new data show 70% of people turning more ‘insular’

Business

History says there’s a 90% chance that Trump’s party will lose seats in the midterm elections. It also says there’s a 100% chance

Now that the 2026 midterm elections are less than a year away, public interest in where things stand is on the rise. Of course, in a democracy no one knows the outcome of an election before it takes place, despite what the pollsters may predict.

Nevertheless, it is common for commentators and citizens to revisit old elections to learn what might be coming in the ones that lie ahead.

The historical lessons from modern midterm congressional elections are not favorable for Republicans today.

Most of the students I taught in American government classes for over 40 years knew that the party in control of the White House was likely to encounter setbacks in midterms. They usually did not know just how settled and solid that pattern was.

Since 1946, there have been 20 midterm elections. In 18 of them, the president’s party lost seats in the House of Representatives. That’s 90% of the midterm elections in the past 80 years.

Measured against that pattern, the odds that the Republicans will hold their slim House majority in 2026 are small. Another factor makes them smaller. When the sitting president is “underwater” – below 50% – in job approval polls, the likelihood of a bad midterm election result becomes a certainty. All the presidents since Harry S. Truman whose job approval was below 50% in the month before a midterm election lost seats in the House. All of them.

Even popular presidents – Dwight D. Eisenhower, in both of his terms; John F. Kennedy; Richard Nixon; Gerald Ford; Ronald Reagan in 1986; and George H. W. Bush – lost seats in midterm elections.

The list of unpopular presidents who lost House seats is even longer – Truman in 1946 and 1950, Lyndon B. Johnson in 1966, Jimmy Carter in 1978, Reagan in 1982, Bill Clinton in 1994, George W. Bush in 2006, Barack Obama in both 2010 and 2014, Donald Trump in 2018 and Joe Biden in 2022.

Exceptions are rare

There are only two cases in the past 80 years where the party of a sitting president won midterm seats in the House. Both involved special circumstances.

In 1998, Clinton was in the sixth year of his presidency and had good numbers for economic growth, declining interest rates and low unemployment. His average approval rating, according to Gallup, in his second term was 60.6%, the highest average achieved by any second-term president from Truman to Biden.

Moreover, the 1998 midterm elections took place in the midst of Clinton’s impeachment, when most Americans were simultaneously critical of the president’s personal behavior and convinced that that behavior did not merit removal from office. Good economic metrics and widespread concern that Republican impeachers were going too far led to modest gains for the Democrats in the 1998 midterm elections. The Democrats picked up five House seats.

The other exception to the rule of thumb that presidents suffer midterm losses was George W. Bush in 2002. Bush, narrowly elected in 2000, had a dramatic rise in popularity after the Sept. 11 attacks on the World Trade Center and the Pentagon. The nation rallied around the flag and the president, and Republicans won eight House seats in the 2002 midterm elections.

Those were the rare cases when a popular sitting president got positive House results in a midterm election. And the positive results were small.

In the 20 midterm elections between 1946 and 2022, small changes in the House – a shift of less than 10 seats – occurred six times. Modest changes – between 11 and 39 seats – took place seven times. Big changes, so-called “wave elections” involving more than 40 seats, have happened seven times. In every midterm election since 1946, at least five seats flipped from one party to the other. If the net result of the midterm elections in 2026 moved five seats from Republicans to Democrats, that would be enough to make Democrats the majority in the House. In an era of close elections and narrow margins on Capitol Hill, midterms make a difference. The past five presidents – Clinton, Bush, Obama, Trump and Biden – entered office with their party in control of both houses of Congress. All five lost their party majority in the House or the Senate in their first two years in office. Will that happen again in 2026? The obvious prediction would be yes. But nothing in politics is set in stone. Between now and November 2026, redistricting will move the boundaries of a yet-to-be-determined number of congressional districts. That could make it harder to predict the likely results in 2026. Unexpected events, or good performance in office, could move Trump’s job approval numbers above 50%. Republicans would still be likely to lose House seats in the 2026 midterms, but a popular president would raise the chances that they could hold their narrow majority. And there are other possibilities. Perhaps 2026 will involve issues like those in recent presidential elections. Close results could be followed by raucous recounts and court controversies of the kind that made Florida the focal point in the 2000 presidential election. Prominent public challenges to voting tallies and procedures, like those that followed Trump’s unsubstantiated claims of victory in 2020, would make matters worse. The forthcoming midterms may not be like anything seen in recent congressional election cycles. Democracy is never easy, and elections matter more than ever. Examining long-established patterns in midterm party performance makes citizens clear-eyed about what is likely to happen in the 2026 congressional elections. Thinking ahead about unusual challenges that might arise in close and consequential contests makes everyone better prepared for the hard work of maintaining a healthy democratic republic. Robert A. Strong, Senior Fellow, Miller Center, University of Virginia This article is republished from The Conversation under a Creative Commons license. Read the original article.Midterms matter

![]()

{kind=link}

Have Democrats given up on the Pinellas County Commission?

Trust has become the crisis CEOs can’t ignore at Davos, as new data show 70% of people turning more ‘insular’

TMZ Sports Streaming Live From Newsroom, Join The Conversation!

-

Politics8 years ago

Politics8 years agoCongress rolls out ‘Better Deal,’ new economic agenda

-

Entertainment9 years ago

New Season 8 Walking Dead trailer flashes forward in time

-

Politics9 years ago

Poll: Virginia governor’s race in dead heat

-

Politics8 years ago

Illinois’ financial crisis could bring the state to a halt

-

Entertainment8 years ago

The final 6 ‘Game of Thrones’ episodes might feel like a full season

-

Entertainment9 years ago

Meet Superman’s grandfather in new trailer for Krypton

-

Business9 years ago

6 Stunning new co-working spaces around the globe

-

Tech8 years ago

Hulu hires Google marketing veteran Kelly Campbell as CMO