Business

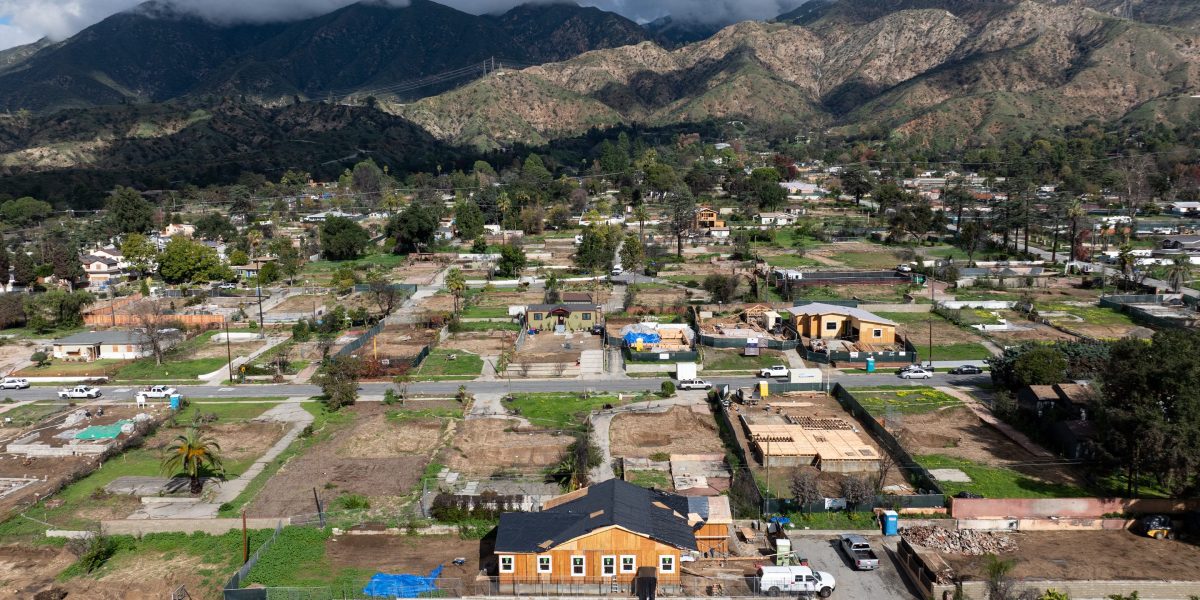

JPMorgan, Citi extend mortgage relief for LA wildfire victims

Business

Rumors are swirling about Venezuela holding $60 billion in Bitcoin—but crypto experts are skeptical

Business

The future depends on copper, but a coming shortage makes it a ‘systemic risk’ to the economy

Business

Walmart’s CEO Doug McMillon out-earns the average American’s salary in less than 20 hours—during a typical 30-minute commute, he’s already made $1,563

Business7 minutes ago

Rumors are swirling about Venezuela holding $60 billion in Bitcoin—but crypto experts are skeptical

Entertainment9 minutes ago

Figure Skater Maxim Naumov Honors Parents In Emotional Tribute Year After Plane Crash

Fashion17 minutes ago

Very Group up for sale again – report

-

Politics8 years ago

Politics8 years agoCongress rolls out ‘Better Deal,’ new economic agenda

-

Entertainment8 years ago

New Season 8 Walking Dead trailer flashes forward in time

-

Politics8 years ago

Poll: Virginia governor’s race in dead heat

-

Entertainment8 years ago

The final 6 ‘Game of Thrones’ episodes might feel like a full season

-

Politics8 years ago

Illinois’ financial crisis could bring the state to a halt

-

Entertainment8 years ago

Meet Superman’s grandfather in new trailer for Krypton

-

Business8 years ago

6 Stunning new co-working spaces around the globe

-

Tech8 years ago

Hulu hires Google marketing veteran Kelly Campbell as CMO