Now he sees an uncanny resemblance — almost an uncanny valley — between the inflation mountain range of the 1970s and ’80s with the inflation wave of 2021 and what may lie ahead for the U.S. economy. Slok wrote in his Daily Spark newsletter for August 31 that upside pressure is mounting on inflation and inflation expectations from tariffs, dollar depreciation and growing disagreement on the Federal Open Market Committee about how to balance rising inflation with slowing employment. (Bank of America Research previously noted that the Fed has rarely cut rates against a backdrop of rising inflation in a note it called “Ghosts of 2007.”)

“The risks are rising,” Slok added, “that we could see another ‘inflation mountain’ emerge over the coming months.”

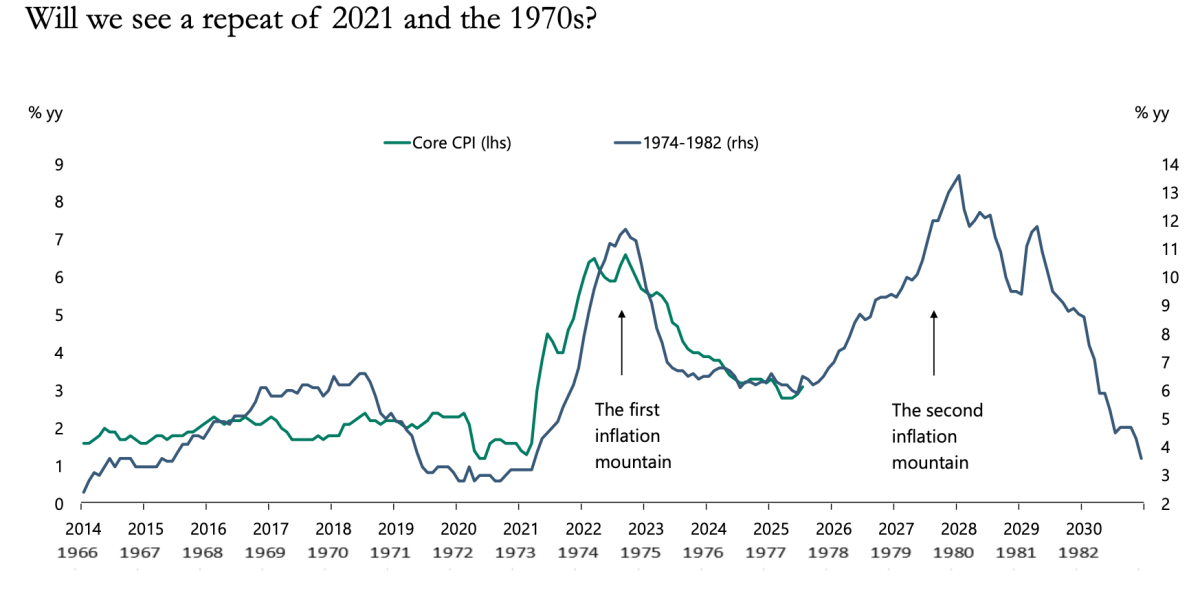

Warning signs emerge

The chart shared by Slok and Apollo juxtaposes the current path of U.S. core CPI with inflation periods from 1974 to 1982, illustrating a close similarity to the inflation wave of 1973/1974 with that of 2021/2022. As Slok’s arrows demonstrate, the first “inflation mountain” of the 1970s was followed by another, taking off around 1978. If the pattern holds, the economy would be due to scale another peak starting almost exactly in the fall of 2025.

Although Slok doesn’t say this in his note, the “first inflation mountain” refers to the initial spike, while the “second mountain” represents the even steeper climb that followed several years later, driven by external shocks and policy missteps.

Mounting inflation fears

These aren’t the first warnings on inflation from Slok. In late August, he argued that Jerome Powell’s choice of words at the Jackson Hole Symposium—saying the labor market is in a “curious kind of balance”—showed that the Fed sees structural distortions from tariffs and immigration policy. If those forces keep inflation sticky and Powell cuts rates, as he’s under pressure from the White House to do, Slok wrote that he could be vulnerable to a 1970s-style “stop-go” policy mistake—the backdrop for the second inflation mountain.

In such a scenario, reminiscent of the ‘70s, if the Fed loosens policy prematurely, inflation could spike, leading to the painful corrective measures seen under Powell’s predecessor Paul Volcker, who hiked rates aggressively and weathered severe, double-dip recessions.

The most recent inflation read, the Personal Consumption Expenditures index, showed prices rising 2.6% in July compared with a year ago, the same annual increase as in June and in line with what economists expected. Excluding the more volatile food and energy categories, prices rose 2.9%, up from 2.8% in June and the highest since February, with Fortune‘s Eva Roytburg reporting that there was a pullback in spending in discretionary categories. The broader Consumer Price Index was flatter than expected at 2.7%, while the Producer Price Index was higher than expected as wholesale prices rose 3.3%, both over the same period.

These warnings come as economists debate the shape of the back half of the 2020s, questioning whether a recession is ahead or the “stagflation” that accompanied the inflation mountains of Slok’s analysis. UBS sees an elevated recession risk from the hard data from the U.S. economy, coming in at 93% in July—although its average recession risk is much lower given its proprietary analysis of other conditions. Still, it forecasts a “soggy” economy ahead, much like Bank of America Research.

JPMorgan was alarmed at July’s shockingly soft jobs report, saying that a slide in labor demand of the magnitude shown in July’s jobs report “is a recession warning signal.” Meanwhile, Mark Zandi, chief economist for Moody’s Analytics, warned in early August the U.S. was on the precipice of a recession, citing much of the same hard data as UBS. More recently, Zandi has put the odds of a recession at 50-50, and he’s said that states representing almost one-third of GDP were either in recession already or at risk of it. Slok’s analysis poses the question: what happens if and when that slams into an inflation mountain?