Business

Google is tightening its ‘Work from Anywhere’ policy: Now a single day will count as a full week

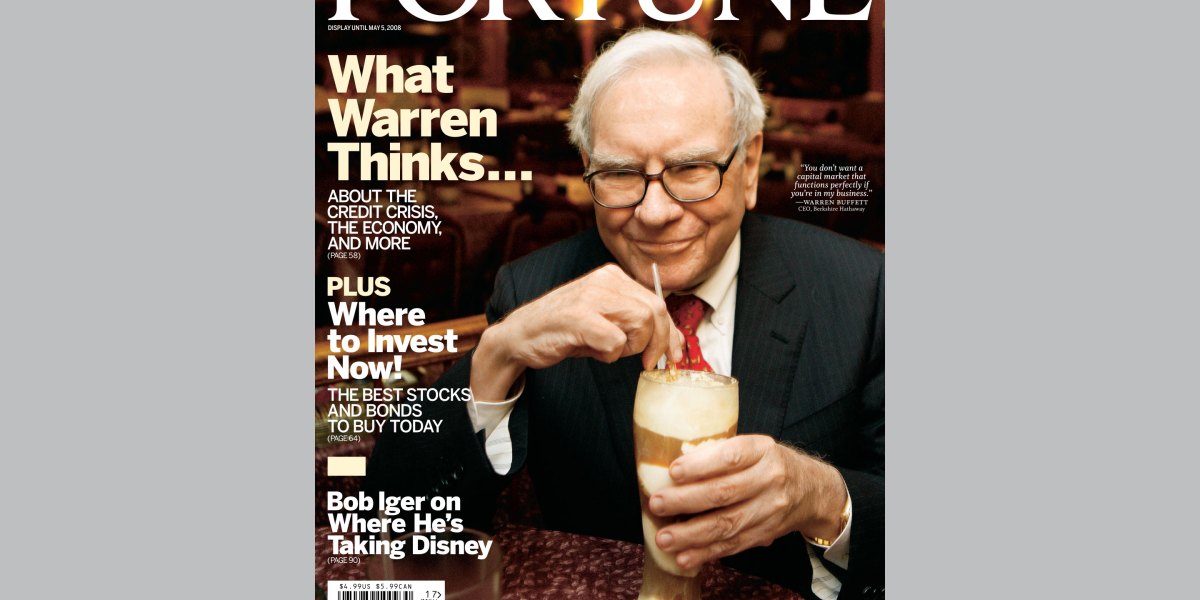

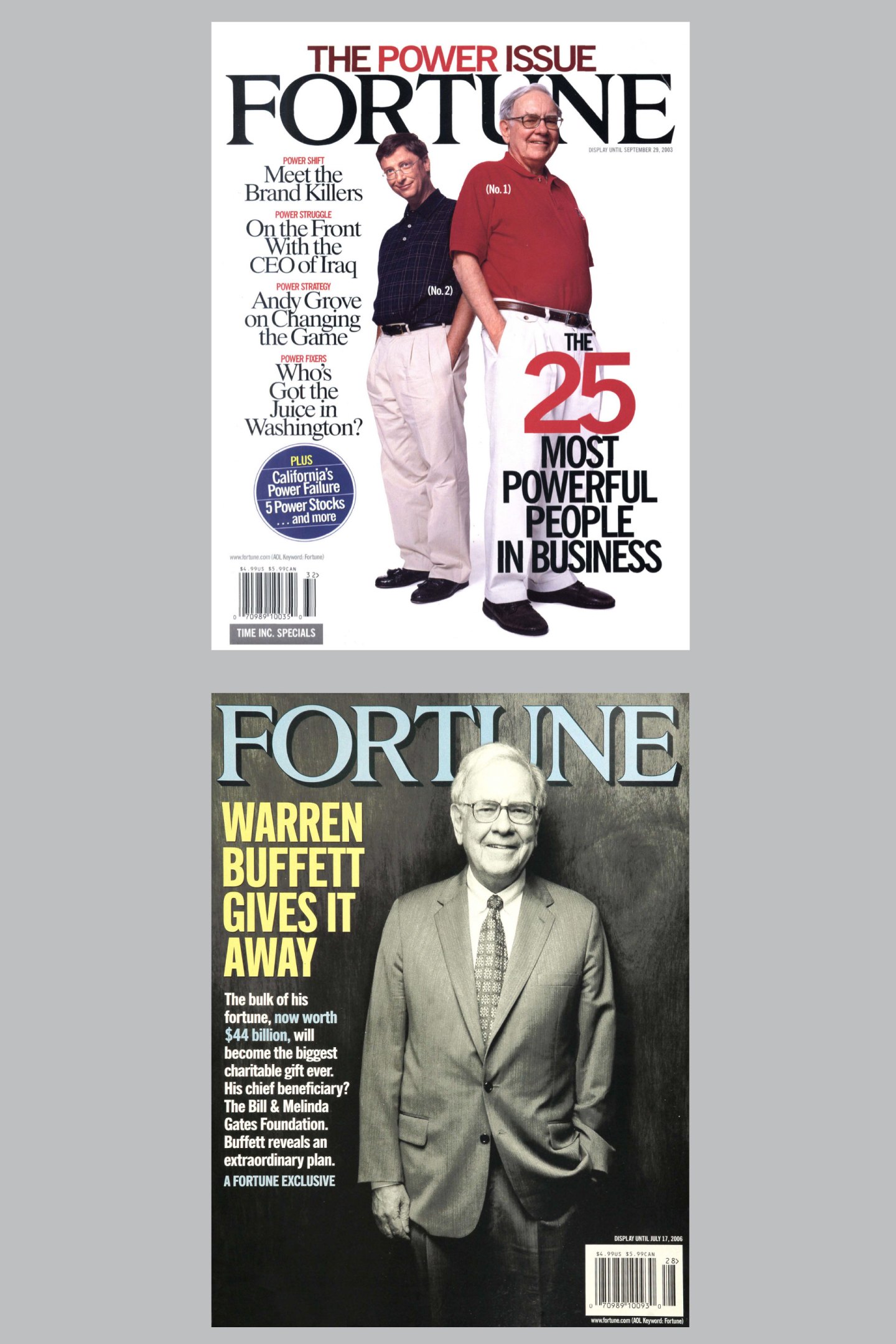

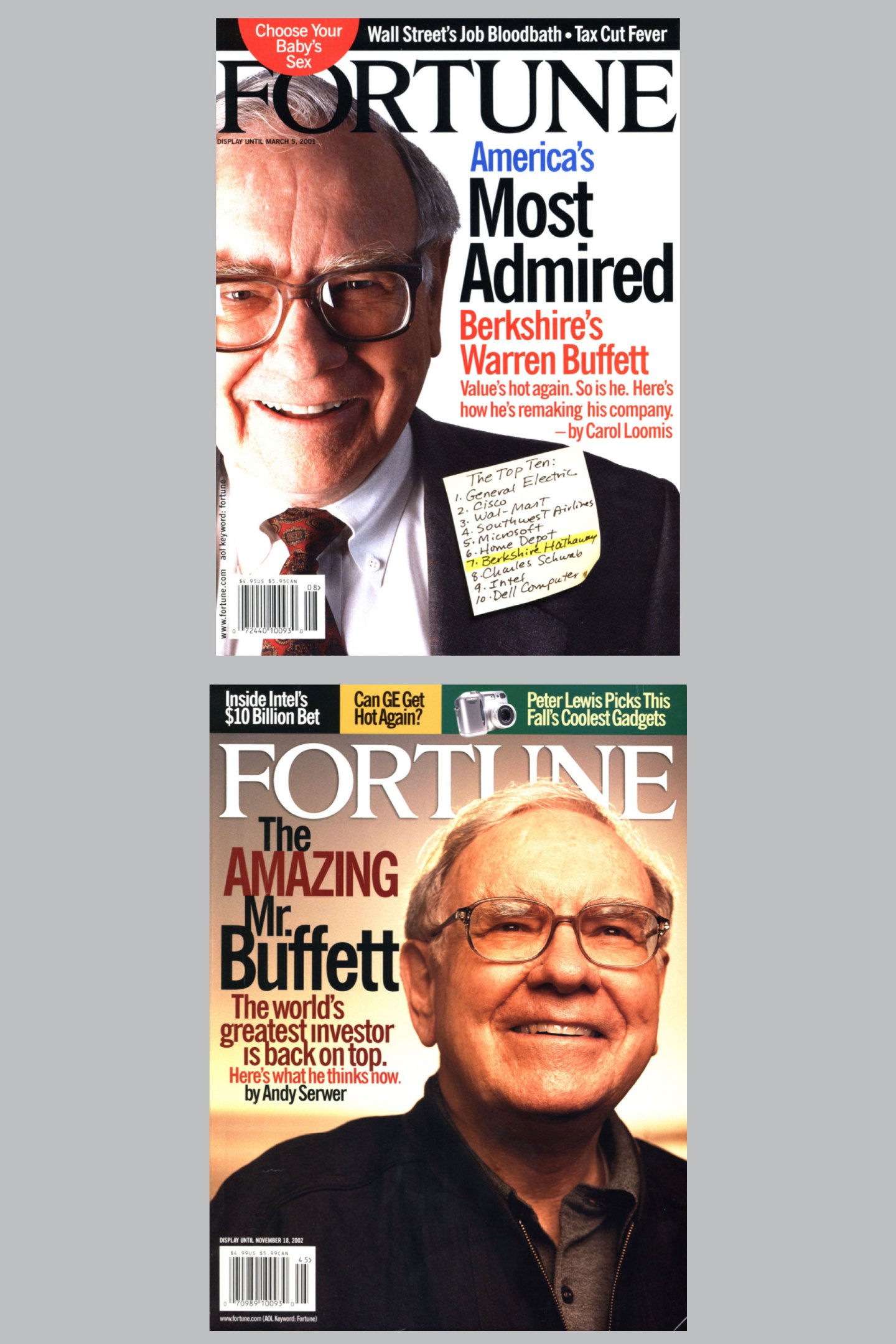

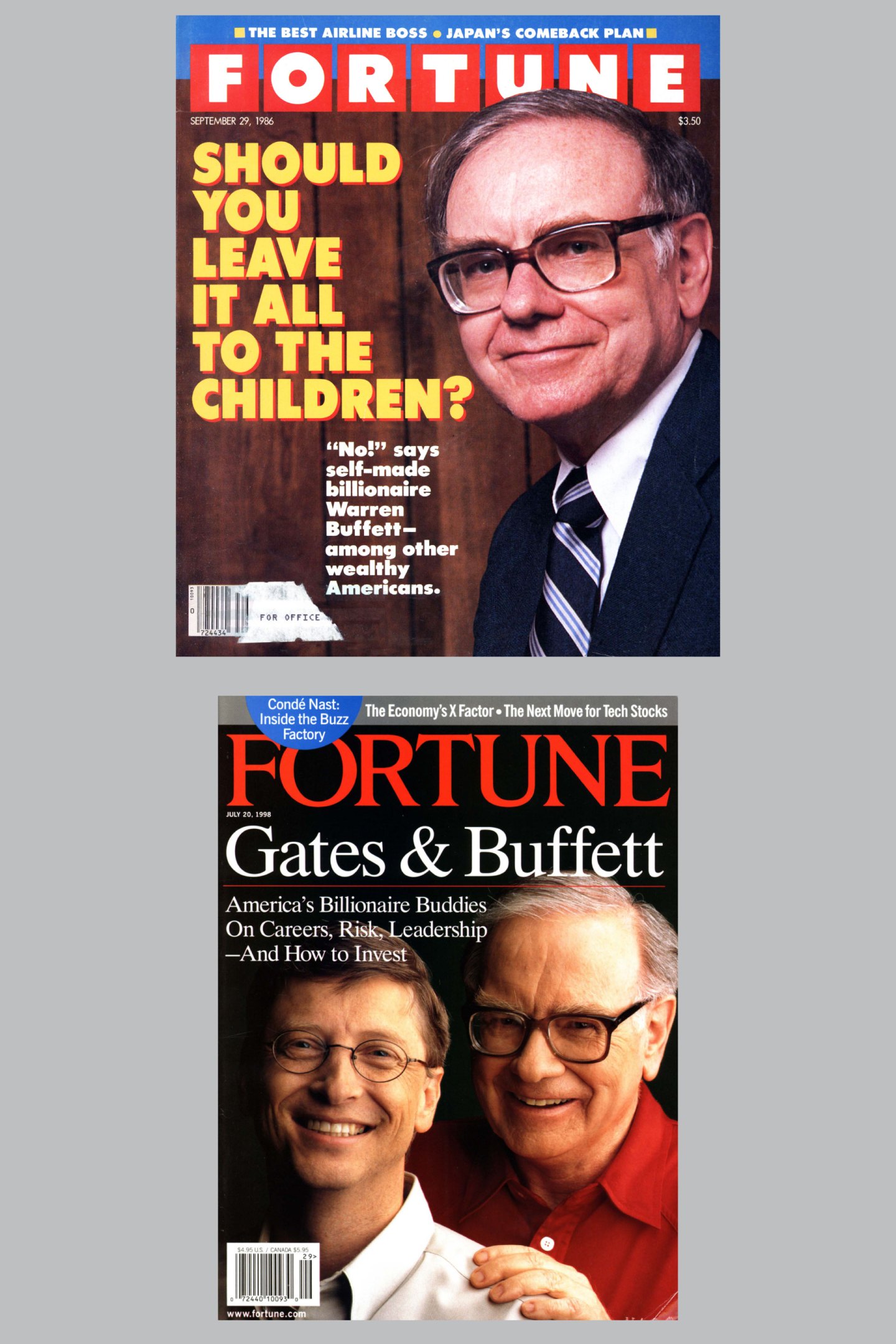

Warren Buffett’s face—always smiling, whether he’s slurping a milkshake, brandishing a lasso, or palling around with fellow multibillionaire Bill Gates—has graced the cover of Fortune more than a dozen times. And it’s no wonder: Buffett has been a towering figure in both business and

investing for much of his—and Fortune’s—95 years on earth. (The magazine first hit newsstands in February 1930; Buffett was born that August.) As Geoff Colvin writes in this issue, Buffett’s investing genius manifested early, and he bought his first stock at age 11. By Colvin’s calculations, over the 60 years since Buffett took control of his company, Berkshire Hathaway, its returns have outpaced the S&P 500 by more than 100 to one.

Buffett has always had a special relationship with Fortune, particularly with legendary writer and editor Carol Loomis, who profiled him many times, and to whom he broke the news of his paradigm-shifting moves in philanthropy in 2006 and 2010. The end of an era is upon us, as Buffett on Dec. 31 will step down from his role as Berkshire’s CEO. We’re grateful to have been along for the ride.

Cover photographs by David Yellen (2009), and Art Streiber (2010)

Cover photographs by Michael O’Neill (2003), and Ben Baker (2006)

Cover photographs by Michael O’Neill

Cover photographs by Alex Kayser (1986) and Michael O’Neill (1998)

Business

Kimberly-Clark exec says old bosses would compare her to their daughters when she got promoted

Eileen Higgins to campaign in Miami with Ruben Gallego ahead of Special Election for Mayor

Warren Buffett: Business titan and cover star

Winner and Loser of the Week in Florida politics — Week of 11.30.25

-

Politics8 years ago

Politics8 years agoCongress rolls out ‘Better Deal,’ new economic agenda

-

Entertainment8 years ago

New Season 8 Walking Dead trailer flashes forward in time

-

Politics8 years ago

Poll: Virginia governor’s race in dead heat

-

Entertainment8 years ago

The final 6 ‘Game of Thrones’ episodes might feel like a full season

-

Entertainment8 years ago

Meet Superman’s grandfather in new trailer for Krypton

-

Politics8 years ago

Illinois’ financial crisis could bring the state to a halt

-

Business8 years ago

6 Stunning new co-working spaces around the globe

-

Tech8 years ago

Hulu hires Google marketing veteran Kelly Campbell as CMO