Business

Down Arrow Button Icon

On Jan. 1, Vitalik Buterin announced a New Year’s resolution for the blockchain he devised way back in 2013. It’s time, he declared, for Ethereum to step up and deliver on its original mission: “To build the world computer that serves as a central infrastructure piece of a more free and open internet.”

Buterin’s message is a timely one. For more than a decade now, Ethereum has offered the tantalizing promise of a global computer, available to anyone, that can be used to create decentralized alternatives to Big Tech’s data-gobbling monopolies. The blockchain popularized smart contracts, and has been a springboard for thousands of projects backed by billions of dollars. It has also spawned legions of mostly fly-by-night imitators.

Despite all of this, the promise of Ethereum always seems just over the horizon. In recent years, the blockchain has come to resemble that can’t-miss sports prospect who can’t quite hack it in the big leagues. Instead of evolving into a popular global computer, Ethereum still feels like a sub-culture where cliques of insiders build esoteric applications for each other. In response, many in the crypto world started betting on other horses like Solana that promised to deliver practical results.

Ethereum’s problem, ironically, has been its idealism. The blockchain has a core community that believes passionately in decentralization, and is mistrustful of anything resembling formal authority. That includes Buterin, who stepped back from his creation several years ago, preferring to let Ethereum find its own path forward.

All of this is admirable, especially in contrast to many recent arrivals on the crypto scene, whose first and only concern is to make a buck. Unfortunately, it has also led Ethereum developers to dither in the face of obvious problems, including congestion and high gas fees. To be fair, the blockchain has made some important fixes—but only after allowing piggy-back chains, known as layer 2s, to siphon off large amounts of revenue and make the crypto landscape painfully complicated.

Now, though, change could be in the air. In the last two years, both BlackRock and JPMorgan Chase have launched tokenized assets that settle directly to the main Ethereum blockchain. This is a testament to how Ethereum remains the gold standard for security and points to a future where it will be the backbone of global finance. The tokenized transactions also legitimize Ethereum’s claim to be a universal computer, and could spur the mainstream adoption of other decentralized applications for social media, identity, and more.

For this to happen, though, the Ethereum community will require Buterin’s ongoing leadership. That’s why his New Year’s Day post is a welcome development. The piece reinforced the primacy of decentralization as Ethereum’s paramount value: “We’re building decentralized applications. Applications that run without fraud, censorship or third-party interference. Applications that pass the walkaway test: they keep running even if the original developers disappear.”

But it also delivered a pragmatic piece of advice to the community seeking to build this decentralized future: Get on with it, already.

Jeff John Roberts

jeff.roberts@fortune.com

@jeffjohnroberts

DECENTRALIZED NEWS

Trump airdrop coming: Yet another Trump token is on the way as Truth Social announced an upcoming drop to its shareholders via Crypto.com. The company added the token will not be transferable and “cannot be exchanged for cash” but could become redeemable for Trump Media discounts. (FT)

Memecoin misery: In a year that saw silver outperform every other asset, Bitcoin notched a 5% decrease in 2025. But the biggest losers of 2026 were memecoins with Dogwifhat down 91%, $TRUMP down 93% and Milei’s $LIBRA down 99%. (WSJ)

Better late than never: The U.S. head of PWC, echoing earlier statements from its Big 4 peers, says the consulting firm decided to “lean in” to crypto in light of the new regulatory environment. The firm is actively providing audits and advice to clients. (FT)

Bitcoin bounces back: The crypto market is off to a strong start in 2026 as Bitcoin climbed over $93,000 and altcoins posted gains even as the economic impact of events in Venezuela remain uncertain. (Bloomberg)

Counting coins: In a key development in corporate accounting, the standard setting body FASB will formally explore whether firms can treat stablecoins as cash equivalents. (WSJ)

MAIN CHARACTER OF THE WEEK

@cipherstein

Ilya Lichtenstein, the mastermind behind the multi-billion dollar Bitfinex hack, is the latest crypto criminal to walk free. He now faces a fate many would regard as worse than prison—resuming domestic life with his rapper wife Razzlekhan.

MEME O’ THE MOMENT

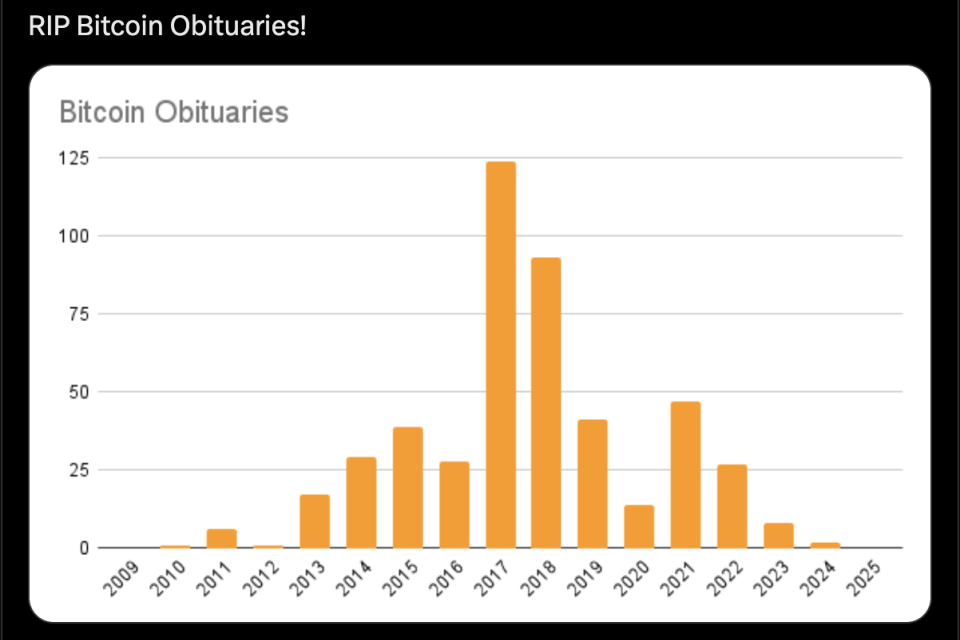

@lopp

It was once fashionable for journalists to seize on price slumps in order to write sneering columns predicting Bitcoin’s demise. These “Bitcoin obituaries” persisted well after the currency’s viability became clear, but now appear to have finally faded altogether.