Business

Coinbase’s new super app Base: summary and review

I’ve covered Coinbase since it was a tiny startup but have never seen anything quite like what the crypto giant rolled out this Wednesday. At a carefully produced stage event in Los Angeles, the company unveiled an app called Base, which is named for Coinbase’s own blockchain, and is billed as a “super app” that offers everything from payments to AI agents to a social network.

All of this isn’t exactly new. For years, Coinbase and other crypto firms have been fiddling with blockchain-based alternatives to services like Facebook and Apple’s App Store. But these offerings came wrapped in a clunky interface that forced users to jump through a variety of crypto hoops, meaning they had little appeal to anyone who was not a blockchain die-hard.

The new Base app is different. It looks and behaves a lot like apps you know, and a single tap brings you to its X-like social network and to pages for trading or sending money. And in a critical decision, Base includes an option to add funds—including the popular USDC stablecoin—using Apple Pay, which makes it accessible to those who don’t want to deal with opening a traditional crypto wallet.

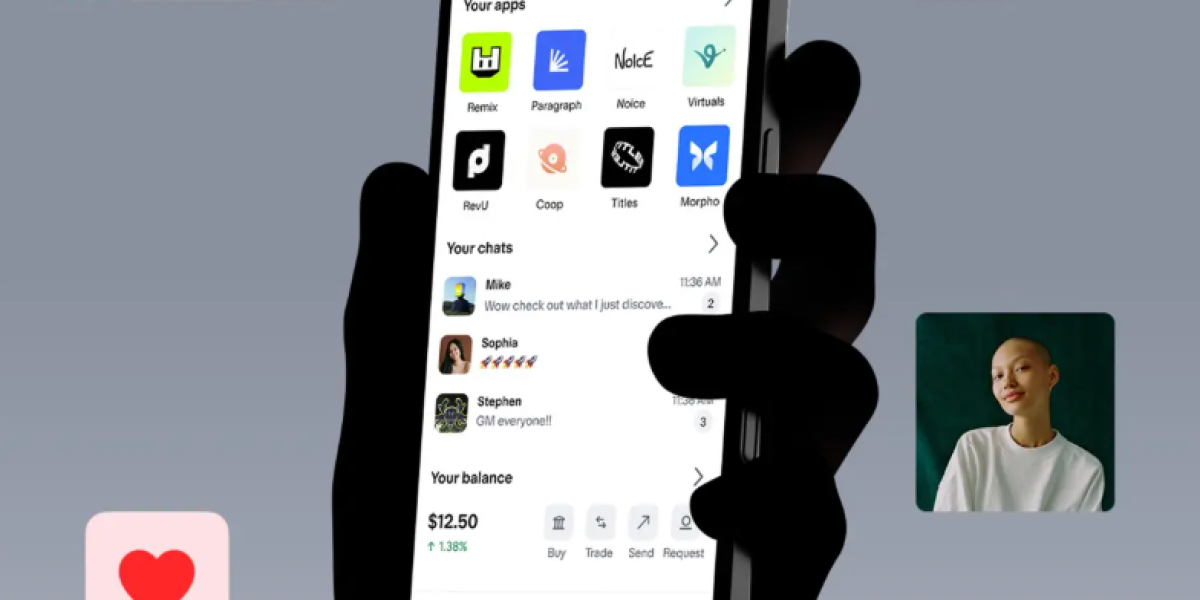

The Base App isn’t entirely new in that it is a rebrand of the company’s existing Coinbase Wallet, which has housed a variety of semi-decentralized services. Base, though, is far easier to use and also solves a long-time branding problem that left users confused about the difference between the core Coinbase app—where you buy and sell crypto—and Coinbase Wallet. Here’s what Base looks like:

For now, Coinbase is only rolling out the Base app to those on a waitlist, and it’s too soon to say if it will get traction among the general public. But the app has a series of features that mean the promise of so-called Web3, which till now has amounted to little more than crypto marketing mumbo-jumbo, could become an everyday reality. Meanwhile, Base could evolve in the medium-term into a serious revenue stream for Coinbase and help it muscle into territory currently held by fintechs and Big Tech firms.

A portable identity for the web

Services like Instagram and Google are hugely popular for a reason. They are free, useful and entertaining but still come at a cost for users, who must surrender control over their personal data as the price for using them. This situation is what led crypto people to tout “Web 3” as an alternative. The idea is that, instead of relying on the likes of Facebook to control your personal data, you control it yourself using decentralized blockchain.

A key part of this Web 3 ideal, which so far has got little traction outside crypto circles, is the idea of a sovereign identity for the internet. For practical purposes, this is a log-in you can use all over the place in the same way you can use your Facebook or Google ID to sign into many websites, but that lets you also connect to contacts, photos and more.

Various crypto firms have been touting versions of a sovereign web identity for years but they failed to catch on. In part, this has been because of a clumsy user experience. But it’s also because these crypto IDs haven’t really been good for much: They don’t cut it as any sort of ID in the real world and, even within crypto realms, there’s not a whole lot you can do with them. So what’s the point?

I put this directly to Jesse Pollak, the Coinbase executive who leads Base, and he acknowledged that the crypto industry has yet to give the public a good reason to use blockchain-based ID. He added, though, that big tech firms have succeeded in making their identity tools very useful to consumers.

“Apple, Google and Facebook have built valuable IDs because the product they offer is valuable,” adding that Coinbase’s goal is to build a service that is equally valuable on a day-to-day level.

This value, Pollak says, will come if the new Base super-app can take off and become part of millions of consumers’ daily online life. He also noted that governments are getting better when it comes to the technology of ID, pointing to recent innovations like state DMVs issuing smart drivers licenses, and passports containing NFC chips. Pollak thinks that, in time, this will open the door to developers building applications that can supply a government-issued credential in situations that require it.

All of this could lead portable, blockchain-based identities to move from the fringe to more mainstream uses. This could include more consumers encountering Base’s sign-on offering alongside ones from Apple and others like this:

A new revenue stream for Coinbase

Coinbase’s new Base offering is an ambitious attempt to put a crypto offering at the center of consumers’ daily lives. The effort is also not cheap. The company has not only invested millions building and developing the app, but is also spending heavily on marketing costs such as the Los Angeles launch, which included a roof-top party for hundreds of Base partners and fans.

This could all pay off for Coinbase, though, if the app achieves the sort of viral growth that Pollak says it’s shooting for. While the company hasn’t explained the revenue strategy for Base, it’s easy to discern two opportunities.

The first would come from more users becoming exposed to Bitcoin and other cryptocurrencies, and buying from Coinbase’s exchange. This would help juice the trading revenue that has long been the company’s bread and butter.

The other revenue opportunity is more intriguing and potentially much bigger. It comes in the form of using Base to promote the adoption of the USDC stablecoin as a peer-to-peer payment vehicle and, especially, as a currency for online shopping. It’s pretty clear this is where Coinbase is going based on several slides at the L.A. presentation, and from the participation of executives from online shopping giant Shopify, whose CEO sits on Coinbase’s board.

Coinbase is also rolling out incentives for those who use what it calls “Base Pay,” including 1% cashback for USDC purchases.

If Base Pay and other USDC uses catch on, it will directly benefit Coinbase’s bottom line since the company gets a share of the interest from the stablecoin reserves that USDC. That interest has already made significant contributions to Coinbase’s quarterly earnings and, if Base makes USDC more popular, that income stream will keep growing.

All of this, of course, is the best case scenario for Coinbase and Base. Even though the company has finally created a blockchain-based app experience that can hold its own against Big Tech style apps, it must still persuade people to use it. And while it’s too soon to say if Base can achieve mainstream adoption, it’s notable that the audience at the LA event skewed very young, and that the accompanying livestream notched 1.6 million viewers, according to a Coinbase exec.

It also remains to be seen if Coinbase can follow through on its promise to make Base a level playing field where any developer can build. Many developers who built projects on sites like Facebook and Twitter learned the hard way that building on another company’s platform puts them at the mercy of getting snuffed out. Pollak and others at Coinbase are quick to say the decentralized blockchain architecture of Base means this can’t happen but it’s not hard to imagine the company finding ways to favor some projects over others.

Putting aside these doubts, Coinbase investors can also take heart that, as the company grows ever bigger, it is still capable of innovating. I spoke briefly with CEO Brian Armstrong who told me that he thinks often about how to preserve a frontier-style mentality even as a big public company and, that to do so, he has made a point of elevating other founders—including Pollak—to the C-suite as a hedge against bureaucratic complacency.

If Armstrong succeeds at this, and if Base can grow into its outsized ambitions, Coinbase could well be a force in the coming decade not only in crypto but in the broader tech and financial landscape.