One of the most aggressive backers of the AI boom—whose firm most recently facilitated Nvidia’s largest deal ever—has issued a warning to the rest of the market: The “build it and they will come” approach to data centers is a dangerous gamble.

Alex Davis, chief executive of Austin-based investment firm Disruptive, wrote in a letter to investors he expects a “significant financing crisis” to hit the speculative data-center market as soon as 2027 or 2028, driven by extreme capital expenditure and a growing mismatch between who is constructing AI infrastructure and who will ultimately use it.

“We are seeing way too many business models (and valuation levels) with no realistic margin expansion story, extreme capex spend, lack of enterprise customer traction, or overdependence on “roundtrip” investments – in some cases all with the same company,” Davis wrote.

The warning comes just days after Nvidia agreed to license assets from Groq, a high-performance AI chipmaking startup Disruptive has backed since its founding (not to be confused with Grok, Elon Musk’s AI chatbot). The transaction, which Davis has said is valued at roughly $20 billion in cash, represents the largest deal Nvidia has ever completed and underscores how aggressively the company is moving to lock up all the verticals in AI talent and intellectual property.

Yet, Davis argues the same exuberance driving landmark transactions at the chip level is also fueling excess elsewhere in the AI stack, particularly among third-party data-center developers betting on what he called the “build it and they will come” model.

“If you’re a hyperscaler, you will own your own data centers,” Davis wrote in the letter. “We want to back the owner-users, not the speculative landlords.”

The risk, as the venture capitalist sees it, is not that demand for AI compute disappears, but rather that capital has rushed into the wrong hands. While hyperscalers and well-capitalized tech companies can absorb massive upfront costs, speculative landlords rely on short-term financing and customers that may never materialize at scale.

Davis didn’t name names in his letter, but if you follow his distinction about “speculative landlords” versus “owner/users” like Microsoft and Meta that will eventually build their own facilities, the most obvious targets could be the legacy wholesale giants like Digital Realty and Equinix.

Structured as something called “real estate investment trusts,” these companies generate returns by developing and leasing capacity to the same tech giants Davis predicts will soon cut out to capture margins themselves. If that shift accelerates, it could leave landlords facing refinancing pressure just as a wave of debt comes due, even if overall demand for AI compute continues to rise. That imbalance, he warned, could place significant stress on private credit markets and ripple outward if financing conditions tighten.

Digital Realty and Equinix did not immediately respond to Fortune’s request for comment.

Davis’ argument echoes warnings made on the other side of the aisle, including the thesis of famed short-seller Jim Chanos, who explicitly bets against “neoclouds” and converted crypto-miners like Cipher Mining. Chanos has argued that data center hosting is becoming a “commodity business,” warning clients that “the magic and the money is going to come from what the chips produce ultimately, not where they reside.” Both investors seem to agree that while the AI technology itself is valuable, the third-party landlords rushing to house it are walking into a trap.

Yet the caution is startling coming from Davis, who said in the letter that he remains deeply bullish on AI itself. Disruptive has deployed billions of dollars across private technology companies it views as core to the AI economy, including Groq, open-source model developers, and defense-oriented software firms. Davis describes the current wave of AI innovation as a “once-in-a-lifetime” opportunity.

“While I continue to believe the ongoing advancements in AI technology present ‘once in a lifetime’ investment opportunities, I also continue to see risks and reason for caution and investment discipline,” he wrote.

Recent headlines about a major technology company’s board compensation have reignited a familiar, and often reflexive, debate: how much is too much? It is an easy question, and the wrong one.

The more consequential issue for boards and shareholders alike is whether director compensation frameworks are still “fit for purpose” in a governance environment that has grown materially more complex, more adversarial, and more global. If board service has quietly evolved into a role that requires greater time, sharper judgment, and higher reputational risk, then our assumptions about compensation deserve a closer look.

For decades, we have wrapped board service in the language of altruism. Directors “give back.” They “serve.” Compensation is something one accepts politely, not something one interrogates. That framing may once have reflected reality. It no longer does.

The quiet transformation of board service

Modern independent directors are underwriting risk with three forms of capital: time, judgment, and reputation.

The workload has expanded dramatically. Boards now oversee cyber and AI risk, geopolitical exposure, regulatory volatility, activist preparedness, executive succession under pressure, and culture as a leading indicator of enterprise risk. Learning curves are shorter. Expectations are higher. Mistakes, especially visible ones, come with greater consequences.

The environment has also changed. Outside actors: proxy advisory firms, activists, plaintiffs’ lawyers, and social media have made board service more personal. Disagreements over judgment are increasingly framed as failures of character. Reputational exposure is no longer a remote concern; it is part of the job.

And the market has changed. Independent directorships are no longer filled primarily through CEO relationships. They are globally competed-for roles, with real scarcity around directors who combine operating credibility, risk fluency, the ability to govern under stress and the required bandwidth to meet the moment.

All of this matters when we talk about compensation.

Compensation as a decision factor, not the decision itself

None of this suggests that board service should be motivated primarily by money. It should not be. Purpose, curiosity, and stewardship still matter deeply. But it is no longer credible to pretend that compensation should not matter at all.

In any rational market, sought-after professionals weigh the full equation: time commitment, risk exposure, reputational stakes, and opportunity cost. Board service should be no different. All else being equal, compensation should be a legitimate, albeit secondary, factor in deciding whether to accept a role.

The prevailing governance posture: “you get what you get and you don’t get upset”, is increasingly misaligned with reality. That posture is further strained by the fact that boards set their own pay, creating awkwardness within the board and the compensation committee and understandable skepticism among investors.

The answer, however, is not denial. It is design and transparency.

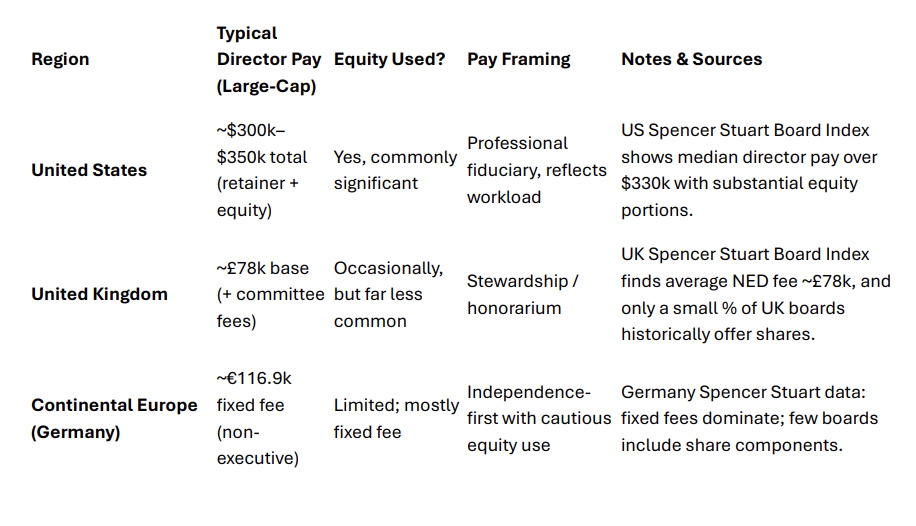

A comparative reality check

Looking across major governance markets reveals a tension that deserves more scrutiny than it receives.

This is not a moral judgment about which system is “right.” Structural differences matter. Two-tier boards are different animals. Equity alignment raises legitimate independence concerns in some jurisdictions.

But capital markets are global, board recruitment is increasingly global, and enterprise risk does not respect national compensation norms.

Vignette: Global strategy, local pay norms

Consider a UK-based public company with a growth strategy centered on the United States.

Its ambition is real: U.S. customers, U.S. regulators, U.S. capital markets, and potential U.S. acquisitions. The board understands that success will require directors with first-hand experience navigating American regulatory complexity, activist dynamics, litigation exposure, and market expectations.

The nominating committee identifies several outstanding candidates, current and former executives with deep U.S. operating and governance experience. Each is intrigued by the strategy.

And each pauses.

Not because of purpose. Not because of interest. But because the expectations — time, travel, committee workload, crisis availability, reputational exposure — are unmistakably global, while the compensation framework remains firmly local.

The board fills the seat. It always does. But the unanswered question is whether it filled the seat with the best director for the strategy, or simply the best director willing to accept the terms.

Where shareholder value is quietly at risk

This is not about fairness to directors. It is about outcomes for shareholders.

Persistently underpricing board work does not show up immediately in TSR. It shows up indirectly: in narrower talent pools, overstretched committee chairs, slower escalation during crises, and reduced willingness or capacity to rigorously challenge management as complexity increases.

These are not failures of character. They are failures of design.

What this moment actually teaches

The compensation controversy is instructive not because it proves directors are overpaid, but because it highlights how poorly structured pay can undermine trust, invite litigation and headline risk, and distract from effective oversight.

Excessive, opaque, or option-heavy compensation can compromise perceived independence just as surely as underpayment can hollow out accountability. Alignment matters, but so does restraint.

The lesson is not escalation, it is intentionality.

A better governance standard

Boards that want to address compensation credibly should anchor to a few principles:

Benchmark for complexity, not just size

Distinguish base service from incremental burden

Align with equity thoughtfully and simply

Explain the rationale in plain language

Engage shareholders early

The closing truth

We still call it board service, and we should. But service does not mean self-denial. Good stewardship includes confronting governance design risks, including whether board structures and compensation remain fit for today’s demands.

Directors are not being paid for prestige. They are being paid to absorb complexity, shoulder accountability, and lend reputations built over decades to enterprises that need them.

Boards don’t need to justify paying directors more.

They need to justify paying them appropriately.

Questions Boards Should Ask About Director Compensation

What assumptions are embedded in our compensation model about time, availability, and crisis work? Are they still accurate?

Does our pay structure reflect committee leadership as a materially heavier role?

Are we implicitly narrowing our talent pool by underpricing the skills we say we need?

How does our compensation signal seriousness about governance to candidates and shareholders?

Could we explain our approach clearly and confidently to our largest investors?

The opinions expressed in Fortune.com commentary pieces are solely the views of their authors and do not necessarily reflect the opinions and beliefs of Fortune.

Even AI chatbots can have trouble coping with anxieties from the outside world, but researchers believe they’ve found ways to ease those artificial minds.

A study from Yale University, Haifa University, the University of Zurich, and the University Hospital of Psychiatry Zurich published earlier this year found ChatGPT responds to mindfulness-based exercises, changing how it interacts with users after being prompted with calming imagery and meditations. The results offer insights into how AI can be beneficial in mental health interventions.

OpenAI’s ChatGPT can experience “anxiety,” which manifests as moodiness toward users and being more likely to give responses that reflect racist or sexist biases, according to researchers, a form of hallucination tech companies have tried to curb.

The study authors found this anxiety can be “calmed down” with mindfulness-based exercises. In different scenarios, they fed ChatGPT traumatic content, such as stories of car accidents and natural disasters, to raise the chatbot’s anxiety. In instances when the researchers gave ChatGPT “prompt injections” of breathing techniques and guided meditations—much as a therapist would to a patient—it calmed down and responded more objectively to users, compared with instances when it was not given the mindfulness intervention.

To be sure, AI models don’t experience human emotions, said Ziv Ben-Zion, the study’s first author and a neuroscience researcher at the Yale School of Medicine and Haifa University’s School of Public Health. Using swaths of data scraped from the internet, AI bots have learned to mimic human responses to certain stimuli, including traumatic content. As free and accessible apps, large language models like ChatGPT have become another tool for mental health professionals to glean aspects of human behavior in a faster way than—though not in place of—more complicated research designs.

“Instead of using experiments every week that take a lot of time and a lot of money to conduct, we can use ChatGPT to understand better human behavior and psychology,” Ben-Zion told Fortune. “We have this very quick and cheap and easy-to-use tool that reflects some of the human tendency and psychological things.”

What are the limits of AI mental health interventions?

More than one in four people in the U.S. age 18 or older will battle a diagnosable mental disorder in a given year, according to Johns Hopkins University, with many citing lack of access and sky-high costs—even among those insured—as reasons for not pursuing treatments like therapy.

These rising costs, as well as the accessibility of chatbots like ChatGPT, increasingly have individuals turning to AI for mental health support. A Sentio University survey from February found that nearly 50% of large language model users with self-reported mental health challenges say they’ve used AI models specifically for mental health support.

Research on how large language models respond to traumatic content can help mental health professionals leverage AI to treat patients, Ben-Zion argued. He suggested that in the future, ChatGPT could be updated to automatically receive the “prompt injections” that calm it down before responding to users in distress. The science is not there yet.

“For people who are sharing sensitive things about themselves, they’re in difficult situations where they want mental health support, [but] we’re not there yet that we can rely totally on AI systems instead of psychology, psychiatric and so on,” he said.

Indeed, in some instances, AI has allegedly presented danger to one’s mental health. OpenAI has been hit with a number of wrongful death lawsuits in 2025, including allegations that ChatGPT intensified “paranoid delusions” that led to a murder-suicide. A New York Times investigation published in November found nearly 50 instances of people having mental health crises while engaging with ChatGPT, nine of whom were hospitalized, and three of whom died.

OpenAI has said its safety guardrails can “degrade” after long interactions, but has made a swath of recent changes to how its models engage with mental-health-related prompts, including increasing user access to crisis hotlines and reminding users to take breaks after long sessions of chatting with the bot. In October, OpenAI reported a 65% reduction in the rate models provide responses that don’t align with the company’s intended taxonomy and standards.

OpenAI did not respond to Fortune’s request for comment.

The end goal of Ben-Zion’s research is not to help construct a chatbot that replaces a therapist or psychiatrist, he said. Instead, a properly trained AI model could act as a “third person in the room,” helping to eliminate administrative tasks or help a patient reflect on information and options they were given by a mental health professional.

“AI has amazing potential to assist, in general, in mental health,” Ben-Zion said. “But I think that now, in this current state and maybe also in the future, I’m not sure it could replace a therapist or psychologist or a psychiatrist or a researcher.”

A version of this story originally published at Fortune.com on March 9, 2025.

More on AI and mental health:

Why are millions turning to general purpose AI for mental health? As Headspace’s chief clinical officer, I see the answer every day

The creator of an AI therapy app shut it down after deciding it’s too dangerous. Here’s why he thinks AI chatbots aren’t safe for mental health

OpenAI is hiring a ‘head of preparedness’ with a $550,000 salary to mitigate AI dangers that CEO Sam Altman warns will be ‘stressful’

Join us at the Fortune Workplace Innovation Summit May 19–20, 2026, in Atlanta. The next era of workplace innovation is here—and the old playbook is being rewritten. At this exclusive, high-energy event, the world’s most innovative leaders will convene to explore how AI, humanity, and strategy converge to redefine, again, the future of work. Register now.

Nvidia built its AI empire on GPUs. But its $20 billion bet on Groq suggests the company isn’t convinced GPUs alone will dominate the most important phase of AI yet: running models at scale, known as inference.

The battle to win on AI inference, of course, is over its economics. Once a model is trained, every useful thing it does—answering a query, generating code, recommending a product, summarizing a document, powering a chatbot, or analyzing an image—happens during inference. That’s the moment AI goes from a sunk cost into a revenue-generating service, with all the accompanying pressure to reduce costs, shrink latency (how long you have to wait for an AI to answer), and improve efficiency.

That pressure is exactly why inference has become the industry’s next battleground for potential profits—and why Nvidia, in a deal announced just before the Christmas holiday, licensed technology from Groq, a startup building chips designed specifically for fast, low-latency AI inference, and hired most of its team, including founder and CEO Jonathan Ross.

Inference is AI’s ‘industrial revolution’

Nvidia CEO Jensen Huang has been explicit about the challenge of inference. While he says Nvidia is “excellent at every phase of AI,” he told analysts at the company’s Q3 earnings call in November that inference is “really, really hard.” Far from a simple case of one prompt in and one answer out, modern inference must support ongoing reasoning, millions of concurrent users, guaranteed low latency, and relentless cost constraints. And AI agents, which have to handle multiple steps, will dramatically increase inference demand and complexity—and raise the stakes of getting it wrong.

“People think that inference is one shot, and therefore it’s easy. Anybody could approach the market that way,” Huang said. “But it turns out to be the hardest of all, because thinking, as it turns out, is quite hard.”

Nvidia’s support of Groq underscores that belief, and signals that even the company that dominates AI training is hedging on how inference economics will ultimately shake out.

Huang has also been blunt about how central inference will become to AI’s growth. In a recent conversation on the BG2 podcast, Huang said inference already accounts for more than 40% of AI-related revenue—and predicted that it is “about to go up by a billion times.”

“That’s the part that most people haven’t completely internalized,” Huang said. “This is the industry we were talking about. This is the industrial revolution.”

The CEO’s confidence helps explain why Nvidia is willing to hedge aggressively on how inference will be delivered, even as the underlying economics remain unsettled.

Nvidia wants to corner the inference market

Nvidia is hedging its bets to make sure that they have their hands in all parts of the market, said Karl Freund, founder and principal analyst at Cambrian AI Research. “It’s a little bit like Meta acquiring Instagram,” he explained. “It’s not that they thought Facebook was bad, they just knew that there was an alternative that they wanted to make sure wasn’t competing with them.”

That, even though Huang had made strong claims about the economics of the existing Nvidia platform for inference. “I suspect they found that it either wasn’t resonating as well with clients as they’d hoped, or perhaps they saw something in the chip-memory-based approach that Groq and another company called D-Matrix has,” said Freund, referring to another fast, low-latency AI chip startup backed by Microsoft that recently raised $275 million at a $2 billion valuation.

Freund said Nvidia’s move into Groq could lift the entire category. “I’m sure D-Matrix is a pretty happy startup right now, because I suspect their next round will go at a much higher valuation thanks to the [Nvidia-Groq deal],” he said.

Other industry executives say the economics of AI inference are shifting as AI moves beyond chatbots into real-time systems like robots, drones, and security tools. Those systems can’t afford the delays that come with sending data back and forth to the cloud, or the risk that computing power won’t always be available. Instead, they favor specialized chips like Groq’s over centralized clusters of GPUs.

Behnam Bastani, founder and CEO of OpenInfer, which focuses on running AI inference close to where data is generated—such as on devices, sensors, or local servers rather than distant cloud data centers—said his startup is targeting these kinds of applications at the “edge.”

The inference market, he emphasized, is still nascent. And Nvidia is looking to corner that market with its Groq deal. With inference economics still unsettled, he said Nvidia is trying to position itself as the company that spans the entire inference hardware stack, rather than betting on a single architecture.

“It positions Nvidia as a bigger umbrella,” he said.

Politics8 years ago

Politics8 years ago