Business

AI isn’t the reason you got laid off (or not hired), top staffing agency says

AI is not the main reason most people are losing their jobs right now; weak demand, economic headwinds, and skill mismatches are doing more of the damage, according to the latest quarterly outlook from ManpowerGroup, one of the largest staffing agencies in the world. While automation and AI are surely reshaping job descriptions and long‑term hiring plans, the first-quarter 2026 employment outlook survey suggests workers without the right mix of technical and human skills are far more exposed than those whose capabilities match what employers say they need.

ManpowerGroup claims its Employment Outlook Survey, launched in 1962, is the most extensive forward-looking survey of its kind, unparalleled in size, scope, and longevity, and one of the most trusted indicators of labor market trends worldwide. Looking ahead to the turn of the year, the survey says employers around the globe still plan to hire, but at a slower pace and with fewer additions to headcount than earlier in the pandemic recovery.

Globally, 40% of organizations expect to increase staffing in the first quarter and another 40% plan to keep headcount unchanged, yet the typical company now anticipates adding only eight workers, down steadily from mid‑2025 levels. Large enterprises with 5,000 or more employees have cut their planned hiring roughly in half since the second quarter of 2025, underscoring just how much large employers are tightening belts even as they keep recruiting in priority areas.

Regional patterns are uneven. North America’s employment outlook has dropped sharply year on year to one of its weakest readings in nearly five years, while South and Central America and the Asia Pacific–Middle East region report comparatively stronger optimism. Europe’s outlook is muted, with only a small decline from last year, suggesting that many employers there are in wait‑and‑see mode rather than embarking on aggressive expansion or deep cuts.

Talent shortage, not job shortage

Despite cooling hiring volumes, 72% of organizations say they still struggle to find skilled talent, only slightly less than a year ago, reinforcing the idea that there is a talent shortage, not a work shortage. Europe reports the most acute pressure, with nearly three‑quarters of employers citing difficulty filling roles, while South and Central America report the least, though two‑thirds of companies in that region are still affected.

The survey suggests shortages are particularly severe in the information sector and in public services such as health and social care. In those fields, three‑quarters of organizations report difficulty finding the right people, even as some workers in adjacent roles complain of layoffs and stalled careers, highlighting the growing gap between available workers and the specific skills employers require.

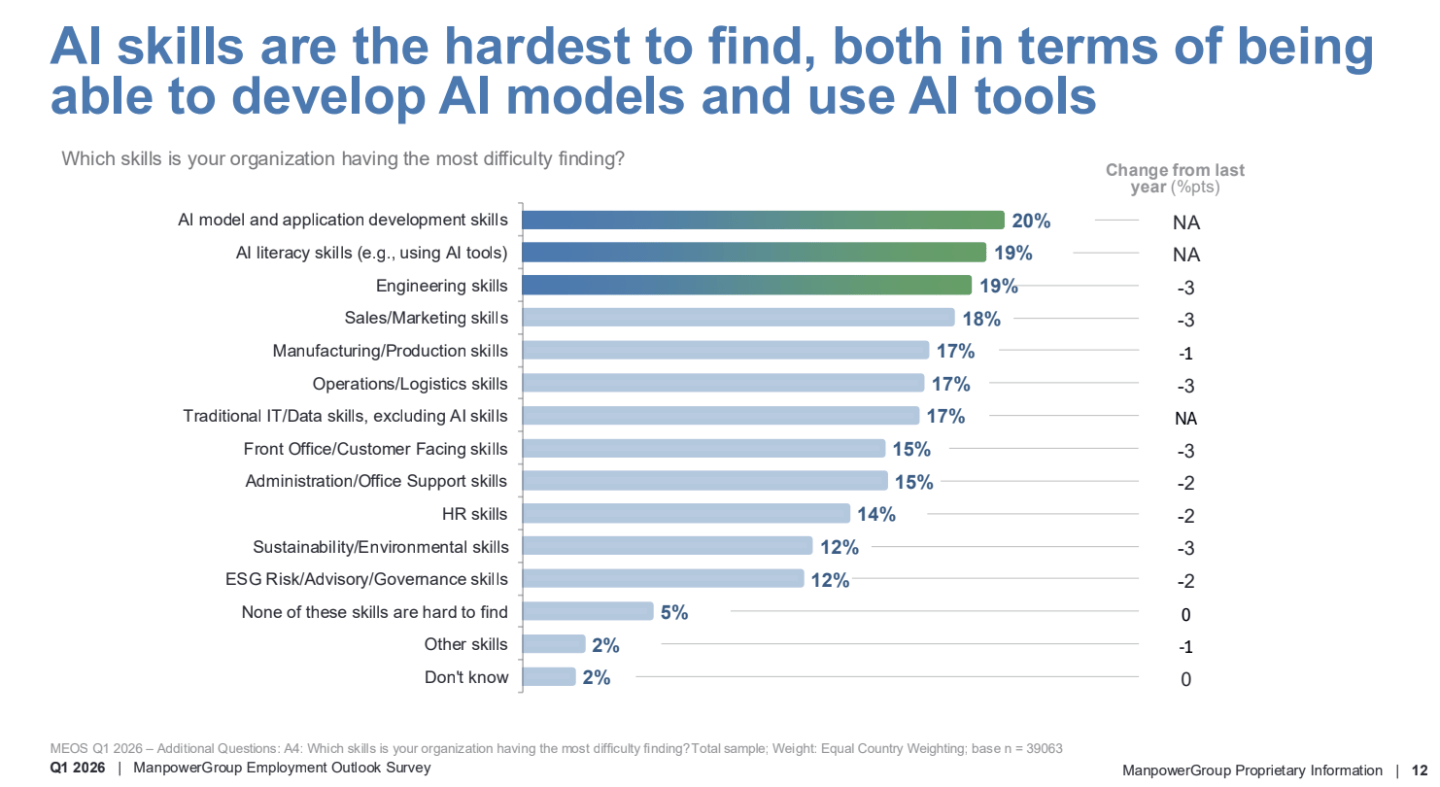

AI skills are scarce, but AI isn’t the axe

If AI were the primary driver of layoffs, employers would not simultaneously report that the hardest capabilities to find are AI‑related. Yet 20% of organizations say AI model and application development skills are the most difficult to hire for, and another 19% say the same about AI literacy, meaning the ability to use AI tools effectively; in Asia-Pacific and the Middle East, these shortages are even more pronounced.

At the same time, when firms do reduce staff, they mostly blame the economy, not automation. Employers who expect to downsize cite economic challenges, weaker demand, market shifts, and reorganizations as the top reasons for cuts, with automation and efficiency improvements playing a secondary role and affecting only certain roles or functions. Changes in required skills appear at the bottom of the list of stated reasons for staff reductions, suggesting that technology is transforming jobs more often than it is eliminating them outright.

Skills mismatch at the heart of layoffs

The report points to a widening skills mismatch as a central fault line in the labor market. Employers say the skills needed for their services have changed, creating new roles in some areas while making other roles redundant, and they struggle to rehire for positions that require capabilities many displaced workers do not yet possess. For organizations that are adding staff, nearly a quarter say advancements in technology are driving that hiring, but they need workers with the right expertise to fill those tech‑driven roles.

Courtesy of ManpowerGroup

Outside of hard technical skills, hiring managers are clear about what they want: Communication, collaboration, and teamwork top the list of soft skills, followed by professionalism, adaptability, and critical thinking. Digital literacy is also rising in importance, especially in information‑heavy sectors, making it harder for workers who lack basic comfort with technology to compete even for nontechnical jobs.

Rather than replacing workers with machines outright, many employers are trying to bridge the gap by retraining the people they already have. Upskilling and reskilling remain the most common strategies for dealing with talent shortages, ahead of raising wages, turning to contractors, or using AI and automation explicitly to shrink headcount.

Larger companies are particularly invested in this approach, with the share of organizations prioritizing upskilling rising along with firm size. Employers in every major region report plans to train workers for new tools and workflows, reflecting the recognition that technology’s rapid advance will demand continuous learning rather than one‑time restructurings.

The big grain of salt for this survey is that it is limited to the next quarter. In the case of a worse long-term downturn, all bets could be off about just how many jobs could be automated with AI tools. This question is beyond the scope of the Manpower survey, but Goldman Sachs economists tackled the issue in October, writing, “History also suggests that the full consequences of AI for the labor market might not become apparent until a recession hits.” David Mericle and Pierfrancesco Mei noted that job growth has been modest in recent quarters while GDP growth has been robust, and that is “likely to be normal to some degree in the years ahead,” noting an aging society and lower immigration. The result is an oxymoron: “jobless growth.”

Until the era of jobless growth fully arrives, though, the Manpower survey suggests that growth will consist of hiring humans who have the right AI skills, whatever those turn out to be.

For this story, Fortune journalists used generative AI as a research tool. An editor verified the accuracy of the information before publishing.