Good morning. Companies earning a spot on the 2025 Fortune Global 500 demonstrated significant momentum this year—including those in the financial sector.

The corporations on this year’s list, released this week, combined to generate $41.7 trillion in revenue in 2024, up 1.8% from the previous year. Together, they employ 70.1 million people, and their revenue represents more than one-third of the world’s GDP.

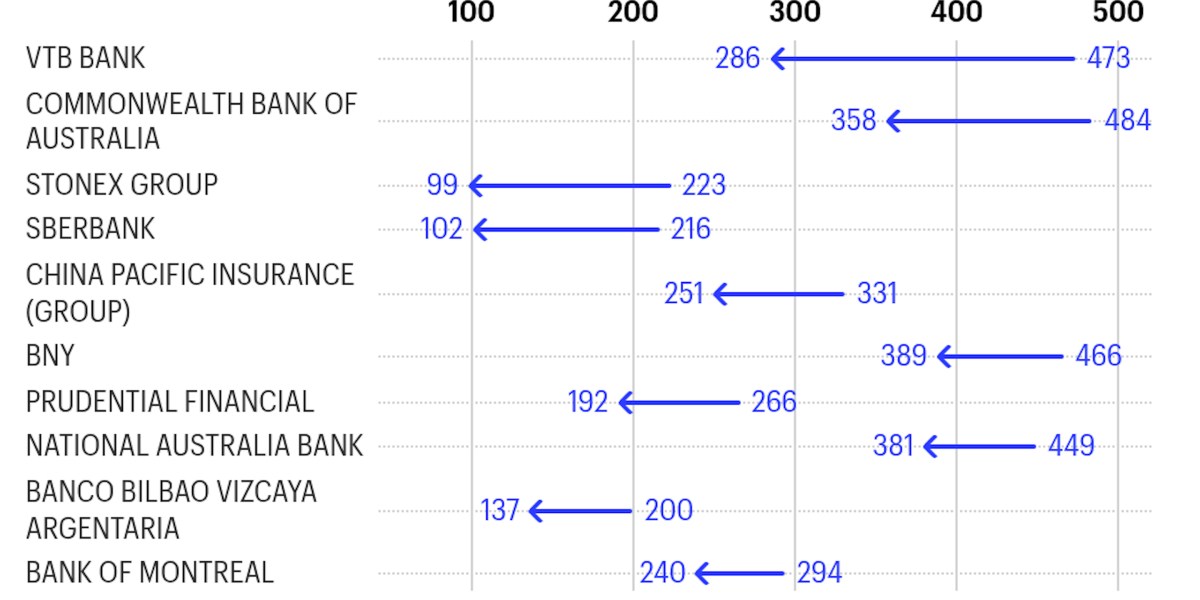

For the 12th consecutive year—and the 20th time since 1995—Walmart is No. 1 on the list. The ranking showed a dominant presence of U.S. companies (138). The U.S. remains ahead of Greater China, which has 130 companies (down three from last year). You can view the complete list here.

Overall, the Global 500 earned $2.98 trillion in profit in its second-most-profitable year ever—and $1 trillion of that was generated by finance companies. Landing at No. 10 is Warren Buffett’s Berkshire Hathaway, the leader in the financial sector.

Also notable: several companies in the financial sector made large advances on this year’s list.

Among U.S.-based companies, banking giant BNY and Prudential Financial made significant jumps on the list. I asked the companies’ CFOs what’s behind this momentum—here’s what they had to say:

Yanela Frias, EVP and CFO of Prudential Financial (No. 192, up 74 spots): “We have seen strong momentum across our market-leading insurance, retirement, and asset management businesses. Our unique combination of global scale, distribution power, brand, and talent sets us apart as we serve 50 million customers worldwide. We are also finding new ways to serve our customers as their needs continue to evolve.

“With more people getting older and facing shifting retirement systems, we are committed to offering flexible retirement solutions that provide protected savings and income strategies to help people live better lives, longer. And, as investors seek a broad range of investment products like private credit and alternatives, we have unified PGIM’s multi-manager model into a single asset management business, including a $1 trillion private and public credit platform. To deliver even stronger performance, we are evolving our strategy, improving execution, and building a high-performing culture.”

Dermot McDonogh, CFO of BNY (No. 389, up 77 spots): “We’re hitting our stride in BNY’s transformation and firing on all cylinders. We’ve built a more connected, agile organization—one that’s breaking down silos and working more closely with clients than ever before. As a company that sits at the center of the global financial system, we have a unique opportunity to help our clients navigate change, unlock opportunity, and operate with greater confidence.

“Our investments in talent, culture, and technology like AI are making us sharper, faster, and more resilient. We’re proud of how far we’ve come, recognize there’s more runway ahead, and focused on continuing to raise the bar.”

Have a good weekend.

Sheryl Estrada

sheryl.estrada@fortune.com

Leaderboard

Fortune 500 Power Moves

Wayne S. DeVeydt was appointed CFO of UnitedHealth Group (No. 3), effective Sept. 2. John F. Rex, who joined the company in 2012 and has been CFO since 2016, will become a strategic advisor to the CEO on the same date. Most recently, DeVeydt, 55, has been a managing director and operating partner at Bain Capital. From 2018-2020, he was chairman and CEO of Surgery Partners, Inc. He joined Anthem, Inc. (now Elevance) in 2005 and served as its CFO from 2007 to 2016. Before joining Anthem, DeVeydt served as a partner with PricewaterhouseCoopers LLP.

Every Friday morning, the weekly Fortune 500 Power Moves column tracks Fortune 500 company C-suite shifts—see the most recent edition.

More notable moves this week:

Justin Plouffe was promoted to CFO of global investment firm Carlyle (Nasdaq: CG), effective Jan. 1, 2026. Plouffe most recently served as deputy chief investment officer for Carlyle Global Credit. He has been with Carlyle for more than 18 years. Justin will succeed John Redett, who will continue serving as CFO through the end of the year.

Kristen Actis-Grande, EVP and CFO of MSC Industrial Supply Co. (NYSE: MSM), has decided to step down from her position, effective Aug. 8, to become CFO of a publicly traded company. Greg Clark, MSC’s VP of finance and corporate controller, will assume the position of interim CFO following Actis-Grande’s departure. Clark has held various finance positions with the Company since 2003. MSC will be conducting a search to identify a permanent CFO.

Patricia Cobian was appointed CFO of BT Group plc. Cobian will succeed Simon Lowth, who plans to retire after nine years in the role. Cobian is currently the CFO at Virgin Media O2. She will join the BT Group board and its executive committee in the summer of 2026, with Simon to retire following a transition period.

Raymond Rindone was appointed CFO of Sunwest Bank. Rindone has more than three decades of experience in the financial services and banking industry. Before joining Sunwest Bank, he served as deputy CFO and head of corporate finance at Banc of California. Earlier in his career, he was deputy CFO at City National Bank.

Eyal Bar was appointed CFO of security startup Chainguard. Bar brings to Chainguard more than 16 years of financial and operational leadership experience from high-growth technology companies. He previously served in senior finance roles at global companies, including Monday.com, steering the company through its Nasdaq IPO, as well as Motorola Solutions, Ernst & Young, and Wix.com.

Jeff Glajch, CFO of Orion S.A. (NYSE: OEC), a global specialty chemicals company, intends to step down early in the fourth quarter of 2025. The company plans to conduct a comprehensive search to identify a successor. Glajch will continue to support Orion through the end of 2025.

Big Deal

On Thursday, President Donald Trump

signed an executive order modifying “reciprocal” tariffs on dozens of countries. The updated tariffs now range from 10% to 41%.

While there is a baseline tariff of 10% for countries not listed with a specific rate, some partners face much higher rates. For example, tariffs on Canada have increased to 35% and take effect immediately (Aug. 1) for goods not covered by the US-Mexico-Canada Agreement. Many of the new “reciprocal” rates for other countries, however, will come into effect on Aug. 7, providing U.S. Customs time to implement the changes. Trump granted Mexico, the U.S.’s largest trading partner, a 90-day reprieve from higher tariffs as negotiations continue.

Going deeper

Here are four Fortune weekend reads:

“Is eBay actually sexy again as the ecommerce old-timer’s stock surges to an all-time high?” by Jason Del Rey

“Beijing officials warm to the idea of a yuan stablecoin, driven by the ‘fear of missing out’” by Cecilia Hult

“Inside IBM’s rebound: Can CEO Arvind Krishna bring the tech company back to its former glory?” by Sharon Goldman

Overheard

“AI is the elephant in the room.”

—Wedbush Securities analysts wrote in a Friday morning note regarding Apple Inc. “While Apple is expanding its AI investments internally, the reality is it’s not moving the needle and investors’ patience is wearing thin,” according to the analysts. The tech giant

announced its latest earnings on Thursday. Apple set a quarterly revenue record as earnings broadly beat expectations,

Fortune reported.